The most significant hurdle to your custom home isn’t the architectural design or the ground-breaking; it’s the sophisticated coordination required to satisfy the stringent construction loan requirements for land and build in 2026. You likely recognize that the transition from purchasing a pristine lot to initiating a major build is fraught with financial nuances that often feel intentionally opaque. It’s natural to feel a sense of trepidation regarding cash flow interruptions or the complexities of coordinating multiple lending phases while maintaining your project’s momentum.

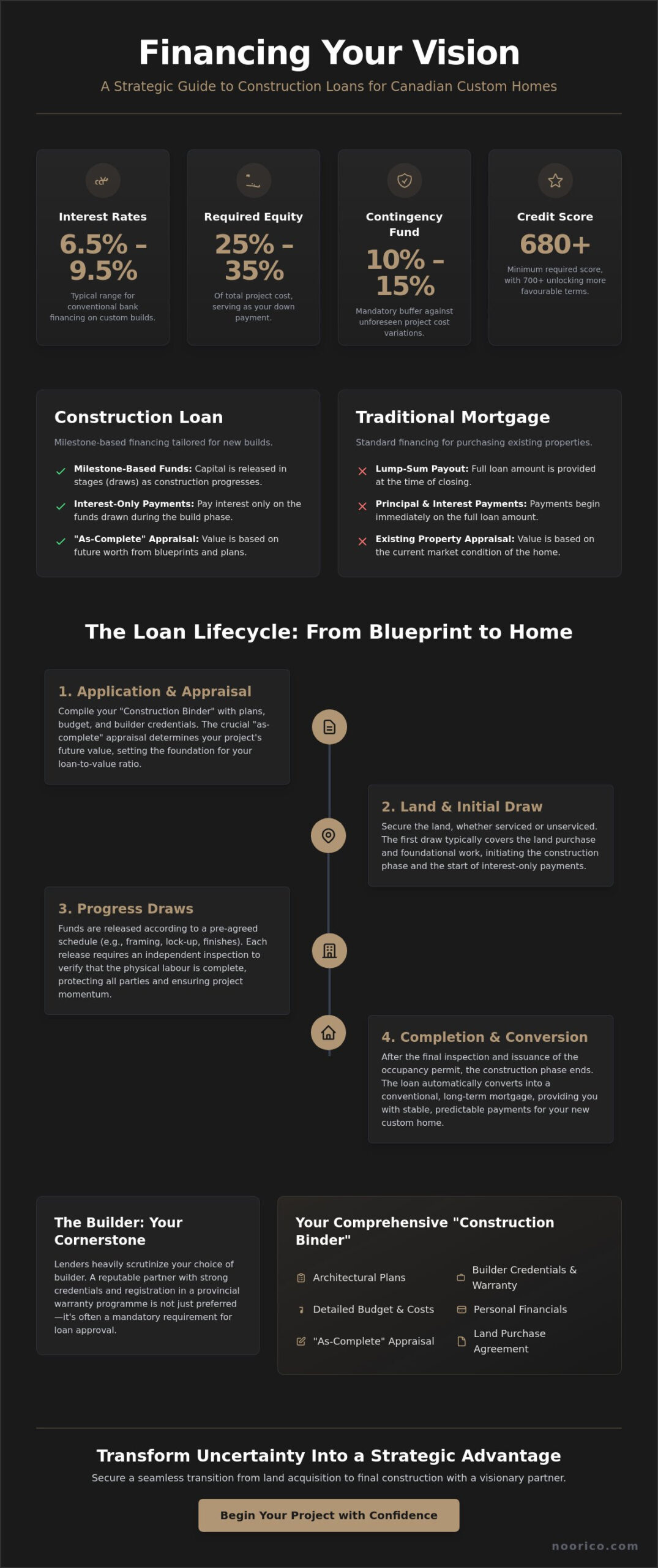

We’ve designed this guide to transform that uncertainty into a strategic advantage, offering a clear path through the progress draw structures and financial benchmarks essential for success. You’ll gain a precise understanding of the current Canadian lending landscape, where conventional rates for bank financing typically range from 6.5% to 9.5% and a 20% down payment remains the standard for distinguished builds. This article details the documentation you need, the mechanics of the draw schedule, and the specific ways a visionary partner can help you secure a seamless transition from land acquisition to final construction.

Key Takeaways

- Master the distinction between traditional mortgages and milestone-based financing to ensure your capital aligns perfectly with your project’s progression.

- Navigate the essential construction loan requirements for land and build by preparing for equity benchmarks typically ranging from 25% to 35% of the total project value.

- Understand the progress draw framework to maintain a steady flow of funds, ensuring each phase of physical labour is verified by independent inspection before capital release.

- Learn why lenders prioritize your choice of builder and how provincial warranty programme credentials serve as a cornerstone for loan approval.

- Discover how to compile a comprehensive “Construction Binder” to move your project from an architectural concept to a financed reality with confidence.

Understanding Construction Loan Requirements for Land and Build Projects

A construction loan is a sophisticated financial instrument tailored for the precise execution of bespoke residential projects. It differs fundamentally from the traditional mortgage products used for existing properties. While a standard mortgage provides a lump sum at closing, a construction loan relies on a milestone-based advancement of funds. This rhythmic release of capital ensures that the lender and the homeowner remain protected throughout the lifecycle of the build. Addressing the construction loan requirements for land and build involves a deep understanding of how these two distinct phases intersect within a single, cohesive financial plan.

The primary objective of this financing is to facilitate Owner-occupancy through a controlled, transparent process. Lenders don’t simply provide capital; they invest in the project’s successful completion. By using a “construction-to-permanent” transition, you can stabilize your long-term financing once the high-intensity phase of construction concludes. This structure offers a safety net, ensuring that your financial strategy is as robust as the home’s foundation.

The Distinction Between Land Acquisition and Build-Out Financing

Lenders view raw land as a higher-risk asset because it lacks the immediate utility of a developed property. In the Canadian market, the distinction between serviced and unserviced land is a primary factor in loan approval. Serviced land, which features existing connections to municipal utilities, presents a much lower barrier to entry. Conversely, unserviced land requires significant infrastructure investment before vertical construction begins. Bundling land and build costs into a single facility provides a strategic advantage, allowing you to synchronize your land purchase with your architectural design and project management timelines while satisfying all construction loan requirements for land and build.

The Lifecycle of a Construction Mortgage

The journey begins with a rigorous application process and concludes only when the final occupancy permit is secured. During the building phase, you’ll typically make interest-only payments on the funds that have been advanced to date. This preserves your liquidity while your project management team executes the labour-intensive build. Once the structure is completed and passes its final inspections, the loan converts to a conventional mortgage. This conversion marks the end of the construction risk period, providing you with a predictable, long-term financial framework for your custom home.

Financial and Personal Eligibility: Qualifying for a Custom Build Loan

Qualifying for a high-value residential project requires more than a standard credit check. Lenders look for a sophisticated profile that demonstrates both financial stability and project foresight. To meet the construction loan requirements for land and build, you’ll typically need a credit score of 680 or higher, though scores above 700 often unlock more favourable terms. Equity requirements are significantly higher than traditional purchases; expect to provide between 25% and 35% of the total project cost as a down payment. This ensures you have a substantial stake in the outcome, mirroring the lender’s commitment to your vision.

Understanding how construction loans work is essential because lenders also mandate a robust contingency fund, usually 10% to 15% of the construction budget. This capital acts as a buffer against unforeseen cost variations, ensuring that material price fluctuations or site-specific challenges don’t stall your progress. It’s a layer of protection that provides quiet confidence to both you and your financial partner throughout the high-intensity build phase.

The Importance of the “As-Complete” Appraisal

The “as-complete” appraisal is the cornerstone of your loan-to-value (LTV) ratio. Unlike a standard appraisal, this process values a home based on architectural design and blueprints before a single shovel hits the dirt. Appraisers analyze high-end comparables to project the future market value of your unique residence. Superior creative achievements in design directly influence this valuation; a more refined architectural plan can lead to a higher appraised value, potentially increasing your available loan amount. If you’re currently refining your vision, our team at NOORICO can help bridge the gap between aspirational design and practical execution.

Financial Ratios and the Debt Service Framework

Lenders utilize Gross Debt Service (GDS) and Total Debt Service (TDS) ratios to assess your capacity to carry the build. These calculations must account for your existing housing costs while simultaneously covering the interest-only payments on the construction draws. A sophisticated loan application should include a comprehensive package of personal financial documents:

- Proof of Income: Recent tax assessments and pay records.

- Asset Verification: Documentation of liquid assets and existing real estate equity.

- The Construction Binder: A detailed collection of permits, architectural plans, and fixed-price contracts.

- Land Documentation: Verification of ownership or the purchase agreement for the lot.

By presenting a transparent and organized financial profile, you reassure the lender that their significant investment is in safe, principled hands. This methodical preparation is what separates a stressful application from a seamless transition to your groundbreaking.

The Progress Draw Framework: How Lenders Manage Construction Risk

The progress draw framework serves as the operational heart of a custom build, replacing the traditional lump-sum disbursement with a rhythmic release of capital tied to specific physical labour milestones. This structure safeguards the lender’s commitment while providing you with a transparent roadmap for project funding. An independent inspector must visit the site at each stage to verify that the work meets the prescribed standards before any funds are released. This level of oversight ensures that the project remains financially viable and physically sound throughout its duration, synchronizing financial draws with physical progress to realize your architectural legacy.

A critical component of the construction loan requirements for land and build is the 10% statutory lien holdback. Required by provincial legislation, this holdback protects you and the lender against potential labour disputes or unpaid subcontractors. It’s vital to align your builder’s contract with the lender’s draw schedule from the outset. When these two schedules mirror each other, you avoid the cash flow interruptions that often stall projects lacking professional oversight. You can review broader construction loan requirements to see how these Canadian standards compare to general industry benchmarks, ensuring your strategy is rooted in global best practices.

Standard Milestone Definitions for Progress Advances

Lenders typically recognize a five-stage advance structure that guides the project from excavation to final occupancy. The first draw usually occurs once the foundation is poured and backfilled, representing the first tangible step in the home’s realization. The “Lock-up” stage is particularly significant in high-end design, as it requires the structure to be entirely weather-tight. For modern architectural designs featuring specialized glazing or expansive window walls, achieving lock-up requires meticulous coordination and persistent dedication. Subsequent draws follow the completion of drywall and the installation of interior finishes, while the final 10% to 15% of the loan is often withheld until the statutory lien period expires.

Managing Cash Flow and Interest During Construction

One of the most efficient aspects of this financing is the interest-only structure, where you only pay interest on the funds actually advanced rather than the total loan amount. Many sophisticated homeowners choose to use their personal equity for the initial stages of construction to minimize interest costs during the early months of the build. To request an advance, you must provide a comprehensive documentation package, including updated budget reports and proof that all municipal inspections have passed. This methodical approach ensures that your financial strategy remains as disciplined as the project management on site, providing a reassuring flow for the duration of the build.

The Builder’s Role: Why Professional Oversight Is a Lending Requirement

When a financial institution evaluates an application for a custom build, they aren’t just looking at your personal balance sheet. They’re assessing the competence, stability, and reputation of the team you’ve chosen to realize the vision. Satisfying the construction loan requirements for land and build necessitates a builder who commands respect through established credentials and a history of superior creative achievements. Lenders prefer a fixed-price contract because it eliminates the volatility of floating costs, providing the structural certainty required to approve a sophisticated budget. This integrated approach reduces the risk premium banks often attach to bespoke projects, moving your build from a speculative venture to a secure, principled investment.

Lenders view the project and the builder as a single entity during the risk assessment phase. A builder’s persistent dedication to their craft is mirrored in their financial transparency and their ability to provide the detailed documentation a bank requires. By choosing a partner with deep-seated reliability, you reassure the lender that their significant investment is in safe hands. This collaborative relationship between the homeowner, the builder, and the bank is what allows a project to move from architectural design to physical reality without financial friction.

Builder Credentials and Provincial Warranty Requirements

Lenders mandate that your builder possesses valid provincial warranty programme credentials. In Ontario, for instance, registration with Tarion is a non-negotiable requirement for new residential builds. These programmes act as a safety net, protecting the lender’s collateral and your investment from structural defects. Even for significant home additions gta, lenders often require professional contractor verification to ensure the expansion meets modern building codes and maintains the property’s value. A builder’s past performance and financial stability undergo rigorous scrutiny, as banks want to see a proven track record of successful completions before advancing capital.

The Strategic Value of Project Management in Financing

Professional project management is the engine that drives the rhythmic release of funds. Lenders require “cost-to-complete” certificates at various stages to confirm that the remaining loan balance is sufficient to finish the home according to the original plans. Your builder’s role is to ensure every milestone is met with precision, preparing the site for the independent inspections that trigger each draw. Architectural oversight acts as a secondary layer of protection, guaranteeing the build adheres strictly to the appraised specifications. This protects the lender’s collateral and ensures your home retains its projected market value. If you’re ready to partner with an established firm that understands these complex financial intersections, explore our custom home building and project management services.

Navigating the Application Process: Preparing for Your Groundbreaking

The final phase of securing your future home is the transition from an architectural concept to a verified financial realization. Navigating this application process requires a visionary mindset that pairs creative foresight with administrative precision. Meeting the construction loan requirements for land and build isn’t merely a box-ticking exercise; it’s the ultimate validation of your project’s creative and financial viability. Because these loans carry a different risk profile for the institution, the approval timeline is often more rigorous and lengthy than a standard mortgage. This period of scrutiny ensures that every pillar of your strategy is sound before the first shovel breaks ground.

A successful application signals to all stakeholders that the project is rooted in decades of industry experience and principled planning. It moves the narrative from abstract inspiration to practical implementation, providing you with the quiet confidence needed to manage a significant investment. This methodical approach mirrors the operational process of the build itself: organized, step-by-step, and entirely transparent.

The Construction Binder: A Masterpiece of Preparation

A masterpiece of preparation, the Construction Binder serves as the definitive record of your project’s intent. It reflects the organizational order of the build itself, signaling to the lender that the project is managed with persistent dedication. A well-organized binder typically includes:

- Architectural drawings and site plans that define the home’s aesthetic and functional footprint.

- Valid building permits and municipal approvals that confirm the project’s legality.

- A detailed budget and fixed-price contract to eliminate financial volatility.

- “Schedule A” specifications, which provide a granular look at the luxury finishes and high-end materials that define the home’s distinction.

Selecting Your Visionary Financing Partner

Choosing the right lender is as critical as choosing your lead architect. While the “Big Five” banks offer stability and competitive rates, they often have more rigid criteria for bespoke residential projects. Private lenders may provide greater flexibility for unique architectural designs or complex land acquisitions, though often at a higher interest cost. When you interview a potential partner, ensure they understand the nuances of the construction loan requirements for land and build and have experience with high-value custom projects in your specific region. This alignment ensures your financial strategy is as sophisticated as the home you intend to create.

The journey from land acquisition to final occupancy is a multi-disciplinary effort that requires a seasoned professional at every turn. By aligning your financial strategy with a firm that offers integrated Architectural Design and Project Management, you ensure that every detail is executed with uncompromising quality. We invite you to begin your transformation with a partner dedicated to enduring professional bonds and superior creative achievements.

Realizing Your Architectural Vision with Financial Precision

Mastering the construction loan requirements for land and build is the foundational step in transforming a sophisticated design into a tangible reality. By navigating the rhythmic nature of progress draws and the rigour of the “as-complete” appraisal, you ensure your project remains on a stable financial footing from groundbreaking to final occupancy. Success in the 2026 lending market depends on the seamless intersection of your financial strategy and your project management team. This methodical preparation ensures that your significant investment is protected by ethical pillars and a commitment to superior creative achievements.

With over 25 years of integrated design-build excellence, NOORICO provides the specialized expertise in high-value project management required to navigate complex residential financing. Our proven track record ensures that every architectural detail aligns with your lending benchmarks, providing you with quiet confidence throughout the high-intensity build. We invite you to begin your journey toward a bespoke residential masterpiece with NOORICO; we remain dedicated to the enduring professional bonds that define your future home. Your vision for a distinguished residence deserves a partner who values precision and accountability as much as you do.

Frequently Asked Questions

Can I get a construction loan for both the land and the build at the same time?

Yes, you can bundle these costs into a single construction-to-permanent loan facility. This integrated approach allows you to synchronize the land acquisition with your architectural design and construction phases under one closing. It streamlines the administrative process and provides a clear financial roadmap from the initial lot purchase to the final occupancy permit.

What is the minimum credit score required for a construction loan in Canada?

Canadian lenders generally require a minimum credit score of 680 to qualify for specialized residential financing. For high-value custom projects, scores of 700 or higher are often necessary to access the most competitive terms and satisfy the construction loan requirements for land and build. This metric reassures the institution of your financial reliability and your capacity for principled capital management.

How much down payment do I need for a land and build project?

You’ll typically need a down payment of 20% to 25% for a conventional project, but bespoke residential builds often require equity between 25% and 35%. This higher threshold reflects the increased risk associated with unique architectural designs and the acquisition of raw land. Maintaining a substantial equity position ensures you have a significant stake in the successful realization of your home.

How do progress draws work for a custom home construction loan?

Progress draws function as a series of capital releases tied to the completion of physical milestones. An independent inspector must visit the site to verify that stages like the foundation, lock-up, and drywall are finished to professional standards before funds are advanced. This rhythmic release protects the lender’s collateral while ensuring a steady flow of liquidity for your project management team.

What happens if there are cost overruns during the building process?

Lenders mandate a contingency fund, usually between 10% and 20% of the construction budget, to handle unforeseen expenses. If cost overruns exceed this buffer, you’re responsible for covering the shortfall out of pocket to keep the loan in balance. This requirement ensures that the “cost-to-complete” remains fully funded throughout every high-intensity phase of the build.

Do I need a building permit before I can apply for a construction loan?

Final loan approval and the disbursement of the first draw require a valid building permit. While you can begin the application process with architectural drawings and a preliminary budget, the lender won’t release capital without legal authorization from the municipality. This step confirms that the project is ready for immediate execution and meets all modern building codes.

Can I act as my own general contractor and still get a construction loan?

Obtaining a loan as an owner-builder is possible but presents a much higher barrier to entry for most borrowers. Lenders typically require a licensed professional with provincial warranty credentials to ensure the project’s success. If you act as your own contractor, expect higher down payment requirements, often between 25% and 30%, and a rigorous review of your past construction experience.

How does a construction loan convert to a traditional mortgage?

The loan converts to a traditional mortgage once the final occupancy permit is secured and the statutory lien period has expired. At this point, the interest-only payments cease and the facility transitions to a standard principal-and-interest structure. This conversion marks the successful transformation of your project from a labour-intensive construction site to a realized residential masterpiece.